Accenture plc

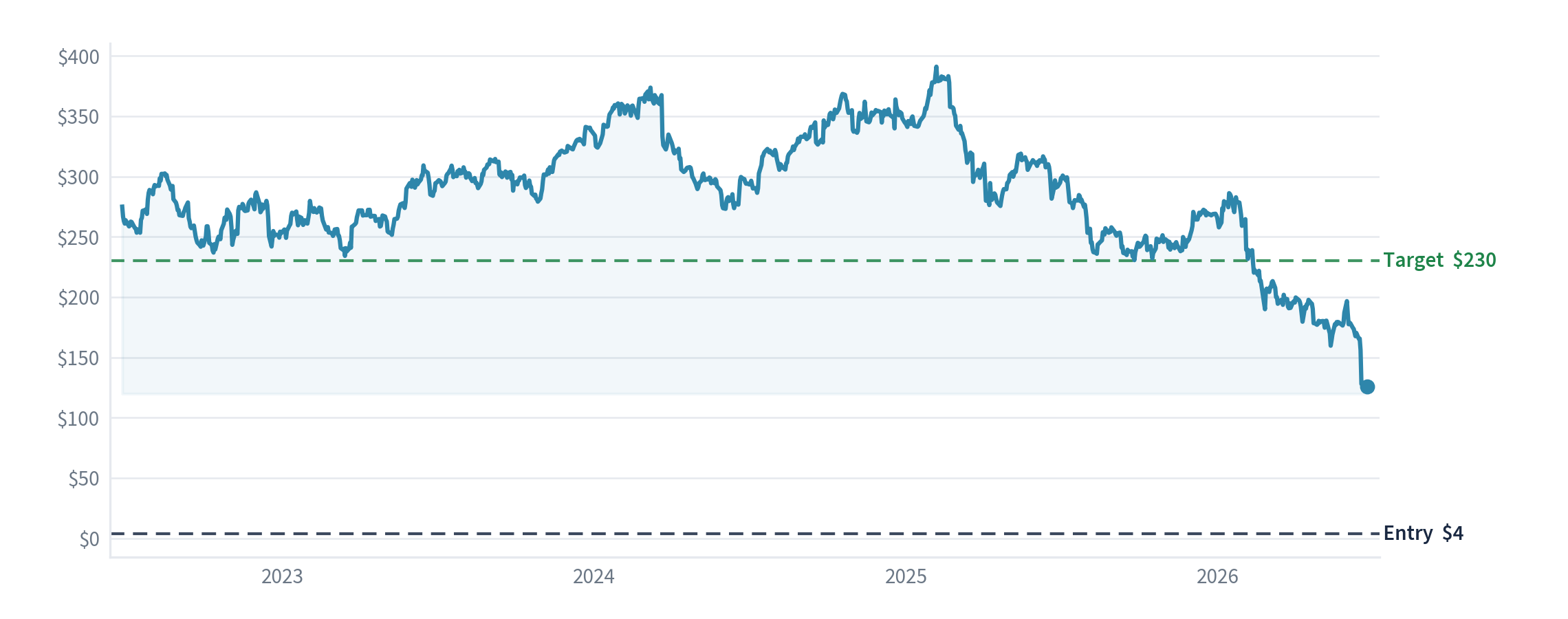

A best-in-class, cash-generative consultancy has been cut roughly 48% from its 2024 high (~$321) to ~$178 on the fear that AI will gut its billable-hours model — yet AI is currently driving record new demand for its help, and the shares pay you about 4% a year to wait and see which way it breaks.

How we would trade it, in plain terms

This one is a watch — but a more comfortable watch than most, because you are paid about 3.7% a year (a rising dividend of roughly $6.50 a share) to be patient. The open question is whether AI grows Accenture's work faster than it shrinks the hours it can bill for; the next year of results will show it. Because the dividend pays you to wait, a small starter to collect the yield while the thesis proves out is defensible — more so than for a business that pays nothing. But we would keep it small and add only on evidence that revenue is re-accelerating with margins holding. We would stay out, or sell, if growth stalls toward zero and profit margins start falling.

What the company does

Accenture is the world's largest technology and management consultancy — about 750,000 people who design, build and run technology and business processes for large organisations. It is paid mostly by time and materials (people × hours × rate), increasingly by fixed-outcome and managed-service contracts, and it has a fast-growing artificial-intelligence practice. It generates a lot of cash, pays a rising dividend and buys back its own shares.

The idea in one sentence

A best-in-class, cash-generative consultancy has been cut roughly 48% from its 2024 high (~$321) to ~$178 on the fear that AI will gut its billable-hours model — yet AI is currently driving record new demand for its help, and the shares pay you about 4% a year to wait and see which way it breaks.

Why it looks cheap

On the company's 2026 guidance (about $13.50 of earnings per share) the shares at ~$178 cost roughly 13 times earnings — reasonable for a business of Accenture's quality, though not especially cheap on that measure. The stronger gauge is cash: after all spending it earns roughly a 12% free-cash-flow return on the business, on a ~15.6% free-cash-flow margin on ~$70 billion of revenue. On top of that you are paid to wait: a 3.7% dividend (just raised 10%, to about $6.50 a share a year) plus buybacks (about $1.7 billion in the latest quarter). The shares are down ~48% from their high.

What the price is implying — our valuation model

At ~13 times earnings with a near-4% dividend, the market is pricing Accenture for little real growth — roughly its soft current guide (about 3–5% growth) fading, with margins under pressure. We model three futures over about two years, built on the company's own guidance:

| Scenario | Chance | What happens | Share worth | Return a year |

|---|---|---|---|---|

| Good | 25% | AI demand converts to revenue, growth re-accelerates, margins hold | ~$300+ | strong |

| Middle | 45% | AI demand roughly offsets the hours it deflates; steady growth, flat margins | ~$230–250 | solid, plus the dividend |

| Bad | 30% | AI shrinks billable hours faster than it adds demand; growth stalls, margins fall | flat-to-down | cushioned by the dividend |

There is also a genuine worst case we will not pretend away: the old people-and-hours model breaks down before the new outcome-based pricing can replace it, and revenue and margins fall together. It is less likely, but real, and it is why we keep the position small if we take one at all. The shape of the bet: you are paid ~4% a year to hold while the better outcomes play out, with a less brutal downside than a no-yield name — which is what makes Accenture interesting here.

What we think the market is missing — and the risk

The market is pricing Accenture as a victim of AI — the billable-hours model getting deflated. The other side: AI is also the biggest source of new demand Accenture has — every large company needs help deploying it, and Accenture is winning that work at scale (its AI order-book is growing fast, up more than 70% over the year). The bears are right that AI cuts the hours per project; the bulls are right that AI multiplies the number of projects. The unresolved question is whether the extra demand outruns the lost hours — and whether AI work is priced at a premium or a discount. For now profit margins are flat and growth is modest, which suggests the new AI work is being absorbed rather than genuinely added — so the optimistic case is still to be proven. If AI deflates hours and pricing faster than it grows demand, the cheap-ish multiple is deserved.

The economic backdrop

Accenture rides the global enterprise and government technology-spending cycle, which is forecast to grow about 13.5% in 2026 — supportive in aggregate. The near-term drags are US federal budget churn and a cautious discretionary-spending mood. The case turns on the AI demand-versus-margin question, not the macro.

The signals we are acting on

A high free-cash-flow yield (cheap on cash) is the load-bearing strand (~12% cash return). It is reinforced by two real capital returns — a growing ~4% dividend and an active buyback — and by a genuine quality moat (top-tier returns on capital, deep, long-standing client relationships) that guards against a value trap, provided the margin question proves manageable.

Channel checks (what we see beyond the filings)

Accenture is exiting more than 11,000 staff who cannot be reskilled on AI, and total headcount fell about 14,000 over the year — but at the same time its AI and data workforce roughly doubled, to about 77,000. Read honestly, that is a deliberate shift of the workforce toward AI, not simple shrinkage — a more constructive signal than pure cuts, though it carries real execution risk. Record new-business bookings point to demand strengthening, which is the strongest objective evidence on the optimistic side.

The investor checklist

- Returns on capital and moat — strong, but people-based. High returns on capital and a deep client-embedding moat. The catch: the profit model is people × hours, exactly what AI deflates, and flat margins on modest growth mean we cannot yet prove the AI shift is adding profit rather than just replacing old work.

- Capital allocation — good and balanced. A rising dividend and a real buyback, plus disciplined bolt-on acquisitions into AI and data.

- Margin of safety — partial. Cheap on cash and paid to wait, but the value hinges on the unresolved margin question, so it is not a clear bargain at today's price.

- Cash quality — strong; balance sheet — sound. Clean cash conversion; low debt / net cash; comfortably funds the dividend, buyback and acquisitions.

- Management — credible. A long record of compounding and disciplined capital return; it raised the dividend 10% into a soft patch — a sign of confidence.

- Insider ownership — modest; no recent open-market insider buying that would lift our conviction.

Management track record

A long, consistent record of compounding revenue and returning capital. Raising the dividend into a cautious macro signals management's own confidence that the AI transition is an opportunity, not just a threat.

What would make us wrong

If AI compresses Accenture's pricing and hours faster than it grows demand — the billable-hours base erodes, the shift to outcome-based pricing squeezes margins, growth stalls near 0–2% and margins fall — then the ~13× multiple is deserved, not cheap, and the dividend alone will not save the return.

What we are watching

- Turns constructive if growth re-accelerates toward high-single digits with margins stable or rising, and AI work is clearly adding to revenue rather than backfilling lost hours.

- Confirms the bear case if growth stays ≤~2% with margins compressing over the next year.

Sources read: Accenture's latest quarterly results and earnings materials (revenue, bookings, margins, guidance, dividend and buyback); its disclosed AI-bookings figures and workforce data; company fundamentals; 2026 sector valuation data; and published bear-case commentary on AI and consulting.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →