Intuit

One of the best software businesses in America has fallen by half from its peak because of a wobble in its smallest, lowest-end product — while its biggest, best parts are still growing by more than 13% a year.

How we would trade it, in plain terms

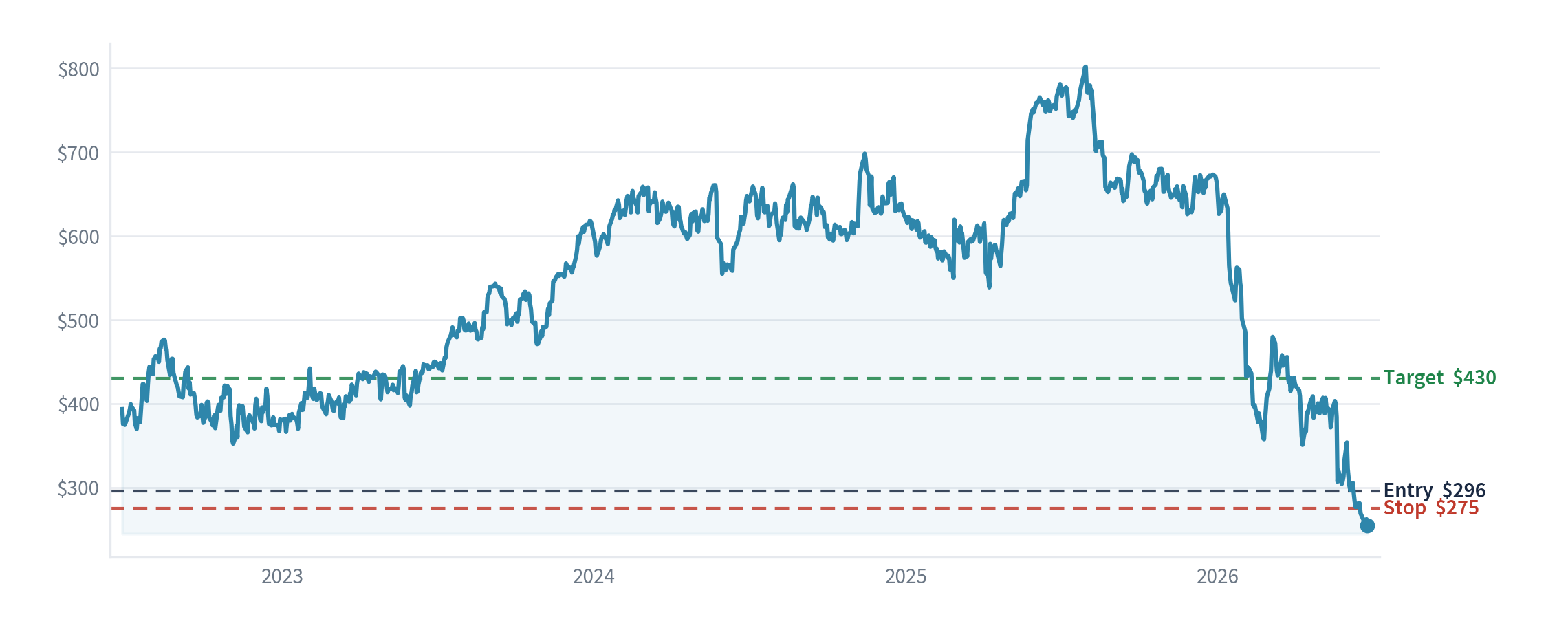

We would buy at the next day's closing price, about $296 a share, sell and take the loss if it fell to $275 (our "stop" — the line that says the idea isn't working), and aim for $430 over 12–18 months. At today's lower price that means risking about $21 a share to try to make about $134 — roughly six to one — though the stop now sits only about 7% below, a tighter line than usual. Confidence: 3.5 out of 5, trimmed from 4 (and the position sized down) because of a fresh legal overhang on TurboTax pricing, explained below.

What the company does

Intuit makes the software households and small businesses use to run their money: QuickBooks (the standard accounting software for small firms), TurboTax (do-it-yourself tax filing), Credit Karma (credit scores and money offers) and Mailchimp (small-business marketing). Most of it is subscription software that customers build their daily work around and rarely switch away from — so the income is steady and very profitable.

The idea in one sentence

One of the best software businesses in America has fallen by half from its peak because of a wobble in its smallest, lowest-end product — while its biggest, best parts are still growing by more than 13% a year.

How shares like this usually behave

Here is our starting point. When a strong, hard-to-leave software business is sold off on fear that a free or AI-powered alternative will destroy it, the fear is usually bigger than the real damage — and history shows it tends to recover once the actual numbers prove the harm is narrower than the headline (the same pattern we describe in our Adobe note). That comfort only breaks in the minority of cases where the new option genuinely and permanently replaces the old product. So the odds are on our side, but the AI-tax question is a real one we have to weigh.

Why it looks cheap

On the company's own guidance (about $23.80 of earnings per share), Intuit at about $296 trades at roughly 12 times earnings — or about 17 times on the stricter all-in measure. For a business growing earnings about 18% a year, that is strikingly cheap, both against its own history (it traded above 30 times for years) and against other quality software: Adobe about 12 times (also marked down), Salesforce about 19, Microsoft about 30. Paying roughly 12 times for an 18%-grower is the sort of price-versus-growth mismatch that usually corrects. The shares fell nearly 50% from their high (a range of about $300 to $814 over the year), almost entirely on worry about the low-end free-tax-filing business — which is only a small slice of profit.

What today's price assumes — and what we think it's worth

We model three possible futures over the next five years. In each we grow the earnings forward, then apply the price-to-earnings ratio we'd expect at the end, to get a fair value:

| Scenario | What we assume | Fair value in 5 years |

|---|---|---|

| Bad case (1-in-4) | AI and free filing genuinely erode the core; growth stalls and the rating stays near today's ~13 times | ~$280 |

| Most likely (1-in-2) | Mid-teens growth continues and the rating partly recovers toward ~20 times | ~$789 |

| Good case (1-in-4) | The AI-expert tier compounds and the fear fades; the rating returns toward ~28 times | ~$1,200 |

Blending those three by how likely we think each is gives an expected return of about 21% a year — the highest in our pool — with a worst-case loss of about 5% if the AI bear is right. Put simply: at 13 times earnings the market is pricing barely any growth, so we do very well if the business merely keeps compounding, while still facing a real, measured downside if free filing and AI bite harder than we expect.

What we think the market is missing

The market has punished the whole company for weakness in its smallest part. Look at what is actually growing over the last year: the QuickBooks small-business arm grew 15%, Credit Karma 15% rising toward 19%, and the online side 19% — and tellingly, the part everyone fears for, expert-assisted tax, is booming: TurboTax Live revenue grew 36% and its customers 38%. These are the profit engines, and they are accelerating, helped by Intuit weaving its own AI assistant into the products. The much-quoted bear case — that AI and free filing will hollow Intuit out — is really about the most price-sensitive do-it-yourself filers earning under $50,000, whom Intuit is steadily moving up into its booming expert tier. A narrow, low-end problem has been mistaken for a threat to the whole franchise.

Two real-world developments support this. First, the US tax authority's free filing programme — the regulatory threat behind much of the fall — was suspended and is not available for 2026, and TurboTax won back about a million free-edition users it had lost to it. Second, Intuit is an active user of AI, not just a target: it is shipping AI helpers inside QuickBooks that save customers around 12 hours a month, and plans to charge for premium AI features from spring 2026.

Does the economic backdrop help or hurt?

Intuit's fortunes follow US small-business health (QuickBooks) and consumer finance (Credit Karma and TurboTax) — a steady US economy helps, a sharp small-business recession would hurt. Falling interest rates would modestly help both new business formation and the value the market puts on the shares. Because Intuit earns in US dollars, the dollar-to-pound exchange rate affects what we make in pounds.

Why we think there's an edge

This is a quality business at a discount — a wide-moat compounder marked down on a narrow fear. The clearest supporting evidence is in how it spends its cash: a genuine buyback that actually reduces the share count, now being done while the shares are cheap, alongside targeted acquisitions. This works whichever way the AI-tax debate ends: even if growth merely holds, cheap shares plus buybacks do the job. We make no claim that insiders are buying — in fact the chief executive sold heavily near the highs (see below), so we lean on the business and the price, not on insider signals.

What other real-world signals show

The outside signals point both ways. Against Intuit: one major broker (Goldman Sachs) cut its rating to sell with a target below today's price, on the AI-tax-competition worry — a serious, well-argued bear case; and a shareholder law firm has opened a securities investigation into how Intuit described its TurboTax pricing this tax season. These investigations are common after a sharp fall and often come to nothing, but it is a fresh overhang — and the reason we trimmed our conviction to 3.5 and sized the position down. For Intuit: a broad set of other analysts (Mizuho, TD Cowen, RBC, Truist, HSBC) see it as resilient to AI and rate it favourably, and the booming expert-tax and small-business numbers back them. It is a genuine two-sided debate, not a one-way loss. (A fuller sweep of this kind of data is still to come.)

The checklist we run every idea through

- How profitable, and how protected — entrenched small-business and tax software, very high recurring revenue and margins, and customers who find it painful to switch away.

- What it does with its cash — steady buybacks that genuinely cut the share count, now at a low price, plus targeted acquisitions.

- Cushion if we're wrong — about 13 times earnings for an 18%-grower; the roughly 50% fall from the highs is the safety margin.

- Are the profits real cash? — yes; strong cash conversion, with a smaller gap between adjusted and all-in earnings than at a serial acquirer (we still note it).

- Is it financially solid? — solid balance sheet; the debt from the Credit Karma and Mailchimp deals is manageable.

- Where we differ, and how we could lose — the market spreads a small-product wobble across the whole firm; we think the engines are fine. We lose if free/AI tax filing genuinely erodes TurboTax and starts pressuring QuickBooks.

- Are managers aligned with shareholders? — long-tenured, capable management, though the chief executive was a heavy seller near the highs (below), so we don't read insider confidence into the price.

Management: do they do what they say?

A strong operating record, with a caveat on share sales. Chief executive Sasan Goodarzi has delivered consistent growth of more than 10% a year, shifted the business to subscriptions, and the company raised its full-year guidance even while flagging the do-it-yourself softness honestly — they do what they say. The caveat: he sold a large amount of stock near the highs (through pre-scheduled selling plans) before the fall, and his two roughly $12bn acquisitions (Credit Karma and Mailchimp) have had mixed results — though he reportedly cancelled planned sales after the drop. A capable operator; just don't read insider confidence into the shares here.

What would make us wrong

The real risk is the idea itself, not the price. If the threat proves bigger than a low-end wobble — if free or AI-powered tax filing genuinely erodes TurboTax and starts pressuring QuickBooks — then the cheap price is deserved. A US small-business recession would also bite. Our discipline: we sell at $275 (about 7% below today's price), roughly where "AI is really hurting the core" would be winning the argument.

What we'll watch to check we're right

- The small-business and online arms keep growing by more than 10% a year through Intuit's 2026 financial year.

- The expert-tax (TurboTax Live) tier keeps booming — it grew revenue 36% and customers 38%.

- Free government filing stays off the table — it could return in a later year.

- The TurboTax-pricing legal probe stays minor — we'd worry if it hardened into a formal action or a regulator joined.

- The premium AI features start earning money from spring 2026, as planned.

- What would make us give up: growth slowing toward the high single figures, QuickBooks itself starting to soften, or clear evidence AI is taking core customers — any of those and we'd downgrade or drop it.

- What would make us re-check the whole case: each quarter's results, any move on government free filing, and fresh evidence on AI tax competition.

Sources: Intuit's results announcements and investor call for its latest (tax-season) quarter and its raised 2026 guidance; the year's quarter-by-quarter trajectory; one major broker's downgrade note and the wider analyst view; the financial figures Intuit files with the US regulator; and market prices for Intuit and its peers (Adobe, Salesforce, Microsoft). Figures are approximate and for context, not advice.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →