JD Sports Fashion

A dominant, cash-generative retailer is priced as if it is in permanent decline, when the more likely story is that its troubles are a passing cycle — chiefly the self-inflicted mess at its biggest supplier, Nike, which is now being fixed.

Where this lands: a watch, not a buy. JD is genuinely cheap and the supplier recovery the whole idea rests on is real and now confirmed by Nike itself. But as of the most recent figures JD's own sales are still falling, so the turn we need is not yet visible where it counts. We want to own this — at the right moment — and that moment is when the recovery shows up in JD's like-for-like sales, not before. Nothing here is advice.

How we would trade it, in plain terms

We are not buying today; we are waiting for one specific thing. JD is cheap for a reason the market can see — its sales are still going backwards — and cheap-with-falling-sales is the classic value trap. One clear, checkable signal would move it from a watch to a buy: JD's like-for-like sales (the change at shops open more than a year) turning positive — the proof that Nike's recovery has finally reached JD's own tills. Until then there is no position. If that turn comes, this would be a patient, twelve-to-eighteen-month holding with a base-case value around 120 pence against roughly 85 pence today, and we would set a stop a sensible distance below our entry at that point.

What the company does

JD Sports Fashion is a shop. It sells trainers (sneakers), tracksuits, hoodies and other sporty, fashion-led clothing — the look people call "athleisure", meaning sportswear worn as everyday fashion rather than for actual sport. It is the largest specialist seller of this kind in the world. It runs about 4,850 stores across the United Kingdom, Europe, the United States and beyond, plus its websites, and it took in £12.66bn of sales in its financial year to the end of January 2026.

It does not make the clothes. It buys them from the big sports brands — above all Nike, but also Adidas, and others — and sells them on at a markup. So it is a retailer, a middleman, not a brand owner. That matters a great deal, and it comes up again. Its own brand, the "JD" fascia with the cougar-head logo, is known for getting first call on the scarce, hyped trainers that sell out — that privileged access to the best product is the heart of what makes JD different from an ordinary clothes shop.

Over the last two years it has spent heavily to grow in the United States, the largest sportswear market on earth, where it was under-represented. In July 2024 it bought Hibbett, an American chain of about 1,179 stores concentrated in the southeast, for roughly $1.1bn (around £0.85bn). Soon after it bought Courir, a French trainer retailer of about 306 stores. Those two deals are why the store count and the headline sales jumped — and why the cash pile shrank, explained below.

The idea in one sentence

A dominant, cash-generative retailer is priced as if it is in permanent decline, when the more likely story is that its troubles are a passing cycle — chiefly the self-inflicted mess at its biggest supplier, Nike, which is now being fixed.

How shares like this usually behave

There are two very different histories for a share like this, and which one you get depends on a single thing. A cheap, out-of-favour retailer with a real, datable catalyst — something specific that breaks the gloomy story — can re-rate hard when that catalyst lands, often 50 to 100 percent or more, because the price started so low and the recovery was not paid for. But a cheap retailer with falling like-for-like sales and no catalyst is the textbook value trap: it looks cheap all the way down, the multiple never recovers, and patient money slowly bleeds. The two look identical at the start. The only reliable way to tell them apart is to wait for the catalyst to show up in the actual sales numbers rather than to buy on the promise of it. That is exactly why this is a watch: the catalyst here is real, but it has not yet reached JD's own results.

Why it looks cheap (with the comparison spelled out)

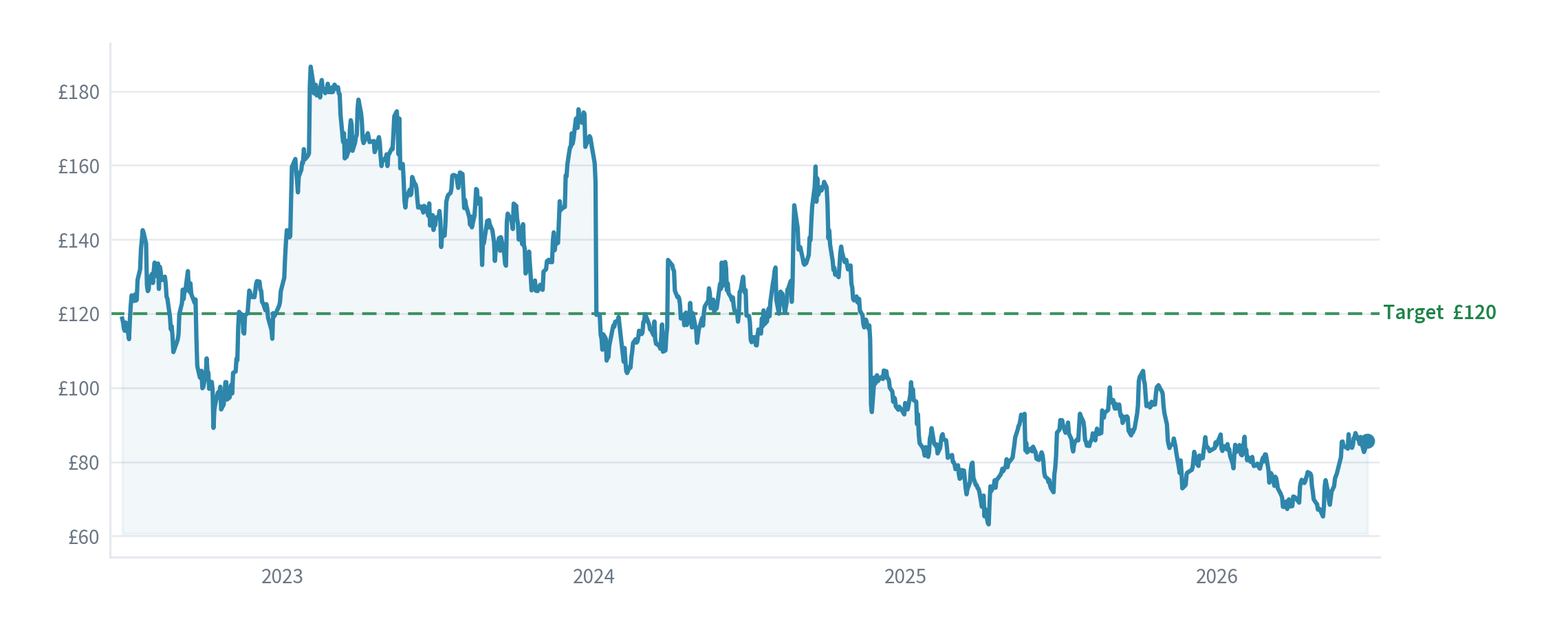

The shares last changed hands around 84.5 pence, which values the whole company at about £4.06bn. That is roughly 60 to 65 percent below the 2021 peak of about 230 pence. On the profit the business reported for its year to the end of January 2026, the price is about 7 times earnings on the company's preferred measure (its "adjusted" profit) — meaning you pay about seven pounds for each pound of annual profit. Measured the stricter way, on the bottom-line profit after every cost (the statutory figure), it is closer to ten times. For comparison, the wider UK market sits around fourteen to fifteen times, and a steady retailer would more typically trade in the low-to-mid teens. So even on the stricter measure the market is pricing JD well below a normal multiple.

How that stacks up against its own kind: the higher-quality US peer, Dick's Sporting Goods, trades on a low-twenties multiple; the wider UK market sits around fourteen to fifteen times; a steady retailer would typically be in the low-to-mid teens. JD, at about seven times its adjusted profit and ten times the stricter statutory figure, sits far below all of them. Some of that discount is deserved — JD is the most supplier-dependent of the group, and its sales are falling. The question is whether all of it is.

The cash backing is the striking part. In that year to 31 January 2026 the business produced £1,309m of operating cash flow after paying its lease costs — up a little on the year before — against that £4.06bn price tag. After all its spending on stores and systems, the spare cash left over (its "free cash flow", the money the business genuinely has free once the bills and investment are paid) was £462m. That is the evidence-backed signal that first flagged the name: a high yield of free cash relative to the price, at roughly eleven pence of free cash for each pound of share price. Crucially, the company itself guides to £460m–£520m of free cash flow again next year, so that level looks maintainable rather than a one-off.

But the cheapness comes with a plain warning the price is reflecting. Profit is falling, not growing. The adjusted profit before tax dropped to £852m from £923m the year before, and the stricter statutory figure fell to £629m from £715m. The profit margin on each pound of sales shrank too — operating profit was 7.0 percent of sales, down from 8.2 percent. And the company has guided for profit to fall again next year, to somewhere between £750m and £850m. So this is a genuinely cheap price, but it is cheap on a business whose profits are still going backwards — which is exactly why the central question (a passing cycle, or permanent decline?) decides everything. One honest note on the cash: part of the jump in free cash flow (to £462m from £339m) came from the company cutting its investment spending — from £515m to £401m — rather than from the underlying cash flow growing, so it flatters the picture a little and is worth watching.

What today's price assumes — and what we think it's worth

Turn the price around and read it backwards. At about 85 pence the whole company is worth about £4.06bn. Set that against the £460m–£520m of free cash the company expects to keep earning each year, and you are paying only about eight times its annual free cash. Put another way: for today's price to be fair — at a 10 percent required return — JD's cash flows would have to shrink by roughly two percent every year, forever. The market is not pricing a wobble or a bad couple of years; it is pricing slow, permanent decline.

That is a demanding thing to assume about the world's largest specialist in its field. A business that merely held its cash flows flat — no growth at all, just steady — would be worth somewhere from the low 100s of pence (valuing those flat cash flows at a 10 percent return) up to about 150 pence (on a normal multiple of its earnings), either way well above today's 85. So the price is not asking "will JD grow?"; it is asking "will JD decline forever?" — and that is the bet we think the market is over-pricing.

Here is how the next three years could play out, with what each case needs and what it would be worth:

| Scenario | What has to happen | ~Fair value | ~3-yr return | Our odds |

|---|---|---|---|---|

| Bear — decline is structural | Nike's recovery helps Nike more than JD; JD's core keeps shrinking; margin slips from 7.0% toward 6%; profit drifts to ~£700m; and — what the market does to a confirmed value trap — the multiple derates further on the falling earnings | ~60p | −29% | 45% |

| Base — cyclical trough, gradual mend | Nike's renewed allocations reach JD; like-for-like sales trough and turn roughly flat-to-slightly-positive; margin holds ~7%; profit recovers toward ~£900m by FY28; a modest re-rating to ~8–9× (still below the market) | ~120p | +41% | 40% |

| Bull — full recovery | Hyped product flows back to JD; like-for-likes turn clearly positive; margin rebuilds toward 8%+; profit tops £1bn; the "permanent decline" story breaks and the multiple re-rates to ~12× | ~180p | +112% | 15% |

Weighting those by our odds gives a probability-weighted expected return of roughly +20% over three years — plus a ~1.4% dividend and an ongoing buyback (a rolling £200m a year) steadily shrinking the share count beneath every holder. But notice the shape: on the evidence we have today, the single most likely outcome is the bear case, and it costs about 29 percent. This is a genuinely two-sided bet — a large upside if the recovery lands, set against a real loss if it does not — not the one-way bargain a bare "seven times earnings" makes it sound.

That two-sidedness is the whole reason this is a watch, not a buy. The base and bull cases — where all the upside lives — depend on a recovery that has not yet appeared in JD's own sales. The day group like-for-like sales turn positive, the bear case loses most of its weight, the expected return jumps, and this becomes a buy. Until then, the honest read is: cheap, promising, and unproven.

What we think the market is missing

The market looks at JD and sees three things, all bad: like-for-like sales (the change at shops open more than a year, stripping out new-store and acquisition growth) that are still falling — down 2.1 percent across the year to January 2026, and down a further 2.3 percent in the first quarter of the new year; a long run of disappointments, including two profit warnings inside 2024 (in January, the shares fell around 18 percent in a day; in November, around 14 percent); and a business that depends on one supplier, Nike, for roughly 45 percent of what it sells. Add those up and you get a seven-times-earnings price — the multiple of a company the market believes is in structural, permanent decline.

The variant view — the thing we think the price has wrong — is that the biggest single cause of the pain is not JD at all. It is Nike. From about 2022 Nike chased a "sell direct to the public" strategy, pulling its best product away from retail partners like JD and pushing it through its own shops and app. That starved JD of exactly the scarce, desirable trainers that drive its sales and its margins. It was a Nike decision, and it hurt every Nike wholesaler, JD most of all because it is the most Nike-heavy.

That strategy has now reversed, and this is the strongest part of the case. Nike brought back Elliott Hill as chief executive in October 2024 — a company veteran — specifically to rebuild the wholesale relationships the previous plan damaged. Nike's wholesale sales have returned to growth (up 8 percent in a recent quarter) after years of falling, and Hill has now named JD Sports directly as one of the partner relationships Nike is "accelerating", with JD once again receiving allocations of the scarce, high-demand product it had been starved of. JD's own finance chief, Dominic Platt, said Nike was "doing all the right things" to revive demand. If JD's single most important supplier is deliberately steering its best product back towards JD, the most Nike-exposed retailer is the geared beneficiary — and it is priced for the opposite.

Here is the honest catch, and it is why this is a watch. That recovery is confirmed at Nike but it has not yet shown up at JD. The early US inflection that looked encouraging — like-for-like sales there going from down 1.7 percent to up 1.5 percent late last year — did not carry through: group like-for-like sales were still down 2.3 percent in the first quarter of the new year (the twelve weeks to 25 April 2026), held back by weak footfall and poor weather across the UK and Europe. So the leading indicator turned and then stalled. The supplier is healing; the customer tills have not yet followed. The question the idea turns on is therefore still open: are JD's problems temporary (a Nike cycle plus a post-pandemic sportswear comedown, both mending) or structural (a middleman being slowly cut out)? The evidence leans towards temporary — but "leans" is not "proven", and the proof will be in the like-for-like line.

How the different investors on the desk see it

- The value buyer: seven times earnings, huge operating cash, and a balance sheet back in net cash (£311m at the January 2026 year-end) after the acquisitions — genuinely cheap on the cash it throws off, if the profits hold.

- The quality buyer: the number-one global specialist, with privileged access to the best product and a share of its markets that has been rising — a real franchise, not a commodity shop.

- The short-seller (the kill-shot): 45 percent of sales tied to one supplier is a structural fragility, not a passing cycle; like-for-like sales are still negative a full quarter into the new year; all the headline growth was bought through Hibbett and Courir, masking a core that is shrinking; and retail margins are thin and falling. Seven times earnings, on this view, is the right price for a business being quietly disintermediated.

- The operator on the ground: JD's premium-partner status means it gets the allocations of scarce, hyped trainers that ordinary shops cannot, and Nike's renewed focus on its best wholesale partners flows to JD first — a concrete, near-term tailwind, not a hope.

The short-seller's case is serious and we do not dismiss it; the still-negative like-for-like sales are its strongest card, and they are a fact, not a fear. The whole idea hinges on the temporary-versus-structural question, and the heavy reliance on Nike is the central risk in both directions.

The economic backdrop (does the country/sector help or hurt?)

The backdrop is unhelpful, which is part of why the price is where it is. Both of JD's biggest markets are soft: the UK and US consumer are cautious, footfall on the high street has been weak (the company blamed exactly that, plus poor weather, for the soft start to the new year), and sportswear as a category is still working off the over-buying of the pandemic years. None of that helps the thesis; the recovery has to come from the Nike cycle and JD's own self-help, not from a rising tide.

One specific swing factor is the currency. JD now earns a large and growing slice of its profit in US dollars (the United States is its biggest market since the Hibbett deal) while it reports in pounds. When the pound is weak against the dollar, those US profits translate into more pounds and flatter the results; when the pound is strong, the opposite. The pound has been trading around $1.33–$1.34, roughly mid-range and a touch softer than where it began the year, so currency is broadly neutral right now — neither rescuing nor sinking the numbers. It is worth flagging only because a sharply stronger pound would quietly take some shine off the very US recovery the bull case depends on.

Net: the macro is a mild headwind. The thesis cannot lean on it, and does not.

The signal(s) we are acting on

The first, evidence-backed signal is the high yield of free cash relative to the price — the spare cash the business earns set against what you pay for it. This is the strongest value signal in our own research, and JD screens clearly on it. Because JD is a UK-listed name, we treat that screen as directional only — a reason to look, never a reason to buy on its own.

The rule we hold ourselves to is that a UK name must never ride on the cash-yield signal alone; there has to be a second, independent reason. Here the second strand is a classic "deeply out-of-favour, with an identifiable catalyst" setup: the price embeds permanent decline, and there is a specific, datable trigger — Nike steering its best product back to JD — that, if it reaches the sales line, breaks the decline story. A third, supporting (not load-bearing) point is capital returns: the company is buying back its own shares through a rolling £200m-a-year programme and has lifted its dividend 20 percent — modest against a £4bn company, so we weight it lightly, but it shrinks the share count and signals management's own confidence in the cash. The second strand is real and improving, but it is not yet confirmed in JD's like-for-like sales — and that single unproven link is why the overall signal is a watch rather than a buy.

What we check beyond the numbers

The most telling ground-level signal is not a consumer data point at all — it is the supplier. Nike's chief executive publicly singling out JD as a partner whose allocations it is "accelerating" is a concrete, checkable sign that the product pipeline that drives JD's sales is being refilled, straight from the source that controls it. That matters more for JD than web traffic or app downloads, because JD's edge has always been access to the right product, and access is exactly what is being restored.

The company's own actions point the same way. Moving to a standing £200m-a-year buyback, lifting the dividend, and openly shifting strategy from aggressive store expansion to "efficiency over expansion" are the moves of a management team that believes its cash generation is durable and wants to return it rather than chase more deals — a marked change of tone from the acquisition spree of 2024. Set against that, the read on the demand side is genuinely mixed: footfall has been weak, and the trade press treats JD as a leveraged bet on the Nike recovery rather than a self-driven grower. We have not found a hard consumer-traffic signal strong enough to lean on either way, and we are not going to manufacture one — the honest position is that the supplier-side evidence is encouraging and the consumer-side evidence is, so far, neutral-to-soft.

The investor checklist (the proven-investor tests)

We score every idea against the tests the great long-term investors use. Each gets a plain pass, partial or fail, with the evidence. JD comes out at three passes, four partials and no outright fails — and all four partials point at the same single unresolved question: has the recovery reached the sales line yet?

- Returns on capital / moat — PARTIAL. JD earns good returns on the money tied up in the business and has a real edge: it is the largest specialist sportswear retailer in the world, and its "premium partner" standing with the big brands gets it first call on the scarce, hyped trainers an ordinary shop cannot get hold of. But it is a reseller of other firms' products, so its pricing power is limited — the gross margin (what it keeps after paying for the goods) was flat at 47.0 percent — and the profit margin on sales fell this year to 7.0 percent from 8.2 percent. The moat is genuine but narrow, and it is being tested right now.

- Use of cash / capital allocation — PASS (with a question on takeovers). The buyback is the real thing, not optics. The company spent around £200m buying back its own shares and the share count genuinely fell — the clearest proof being that its long-standing controlling shareholder, the Pentland Group, did not sell into the buyback, and so its stake rose from about 53.4 percent to about 54.9 percent purely because the total number of shares shrank beneath it. The dividend was lifted 20 percent, and the company has now committed to a standing £200m-a-year buyback. The open question is the takeovers: the 2024 purchases of Hibbett (about $1.1bn) and Courir are what produced this year's £119m of write-downs and integration costs, so whether that spending was disciplined or over-reaching is not yet settled. Borrowing is now at a sensible level.

- Margin of safety — PARTIAL. At about seven times the adjusted profit, roughly half the UK market's multiple, with a free-cash yield in the low teens, the shares are visibly cheap against their own history and the market, and the price embeds permanent decline that we doubt. But with profits still falling and the recovery unproven in the sales line, the floor under the value is itself uncertain — the margin of safety is real on paper but not yet underwritten by the numbers turning.

- Cash quality / accounting — PARTIAL. The business turns profit into real cash well: operating cash flow was £1,309m. Two cautions, though. First, the gap between the statutory profit (£629m) and the "adjusted" profit management leads with (£852m) is £223m — almost all of it non-cash (£119m of write-downs, including £93m for under-performing stores and £15m for the Sizeer chain, plus £69m for writing down the value of the acquired businesses); only £4m was an actual cash cost. Second, the headline jump in free cash flow leans partly on cutting investment rather than on the operating cash flow growing. Real cash generation, read with those two flags.

- Balance sheet — PASS. Strong and improving. The company ended the year with £311m of net cash before its shop-lease commitments (up from £52m a year earlier), and total borrowings including those leases fell to 1.4 times profits from 1.7. It comfortably funds its dividend and buyback from its own cash. The balance-sheet strain from the 2024 takeovers has unwound — the worry the bear case raised has resolved.

- Variant perception + "how could we lose?" — PARTIAL. The non-consensus view is clear: the pain is mostly a passing Nike cycle, not the slow cutting-out of a middleman. The way we lose is equally clear, and it is live right now — every region still had falling same-store sales in the last full year (United Kingdom down 3.9 percent, North America down 1.8 percent, Europe down 1.2 percent, Asia-Pacific up just 0.4 percent), group like-for-likes are still negative a quarter into the new year, and management has guided this year's profit down again. So the "trough" the whole idea needs is not yet visible in either the company's results or its own forecast. The variant view is real; it is not yet proven.

- Insider alignment — PASS (with a governance note). Alignment is unusually high. The Pentland Group, the Rubin family's holding company, has controlled roughly 55 percent of JD for decades — an owner with that much of its own wealth in the business is strongly motivated to make it worth more. The flip side is governance: ordinary shareholders ride alongside a family that can outvote them, and any dealings between JD and its controlling owner need watching.

Management track record (do they do what they say?)

Mixed, and improving from a low base. The black mark is recent and real: management set, then twice cut, its profit guidance during 2024 — two profit warnings in one year, each of which knocked the shares double digits in a day. That is a genuine credibility cost, and it is part of why the market now demands to see the recovery rather than take it on trust. We weight that heavily; it is the main reason we want proof in the numbers before acting.

Against it, the more recent record is steadier. The year to January 2026 came in within the guidance management had set, and the company has been candid about the soft start to the new year rather than dressing it up. The strategic shift — from buying growth (Hibbett, Courir) to "efficiency over expansion" plus a standing buyback — reads as a more disciplined, shareholder-aligned stance than the acquisition spree that preceded it, and the finance chief's plain-spoken read on Nike ("doing all the right things") has so far been borne out by Nike's actions. So promise-versus-delivery is rebuilding but not yet re-established. The right posture is the one this note takes: give the strategy credit, but wait for one more clean delivery — a guidance met and the sales line turning — before trusting the recovery with real money.

What would make us wrong

The single thing that breaks this idea is the Nike relationship turning out to be a structural weakness rather than a passing cycle. If Nike's recovery stalls, or if Nike again favours its own shops and app over partners, then JD's biggest dependence becomes its biggest problem, and the cheap price is cheap for a reason. The second danger is the core simply continuing to shrink: like-for-like sales were down 2.1 percent last year and down a further 2.3 percent in the new year's first quarter, and if that does not turn — if the only growth keeps coming from buying other chains — then this is a value trap, cheap all the way down. The shares are already roughly 60 to 65 percent below their 2021 peak, so the market has gone a long way towards pricing the bear case — but not all the way: in our bear scenario there is still roughly 25 to 30 percent more to lose if the core keeps shrinking and the multiple derates further on falling profits. That downside is real, and it is exactly why we wait for proof in the sales line rather than buy the cheapness. Because this is a watch and not a position, the protection for now is simply that we have not bought; a concrete stop would be set at the point we upgrade to a live holding.

What we'll watch to check we're right

- The upgrade trigger (watch → buy): group like-for-like sales turning positive in a quarterly update — the clean signal that Nike's recovery has reached JD's own tills. The next read is the half-year update in the autumn.

- On track: US like-for-like sales re-accelerate, and group like-for-likes climb back towards flat and then positive through the year.

- Off track: like-for-like sales stay negative through 2026, or Nike's wholesale recovery reverses.

- What would make us walk away entirely: a fresh profit warning, or clear evidence Nike is again favouring its own direct channels over partners like JD.

- When we'll re-check: each quarterly trading update, the next full-year results, and any Nike update that bears on the wholesale relationship.

Sources: JD Sports full-year results for the year to 31 January 2026 (published 7 May 2026), including the profit, cash-flow, balance-sheet, dividend and buyback figures, the segment same-store sales, the first-quarter (to 25 April 2026) trading update and the next-year guidance within it; prior-year and interim results; shareholder-register filings on the Pentland Group's stake; Nike's reported wholesale results and its chief executive's commentary naming JD as an accelerating partner; and current market pricing and exchange rates.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →