The Magnum Ice Cream Company

Spin-off forced-selling + a genuine insider cluster

How we would trade it, in plain terms

We are not buying this yet. It's on the watchlist. We'd only act if the company's next results actually prove the cash-recovery story below — until then there's too much we can't confirm.

What the company does

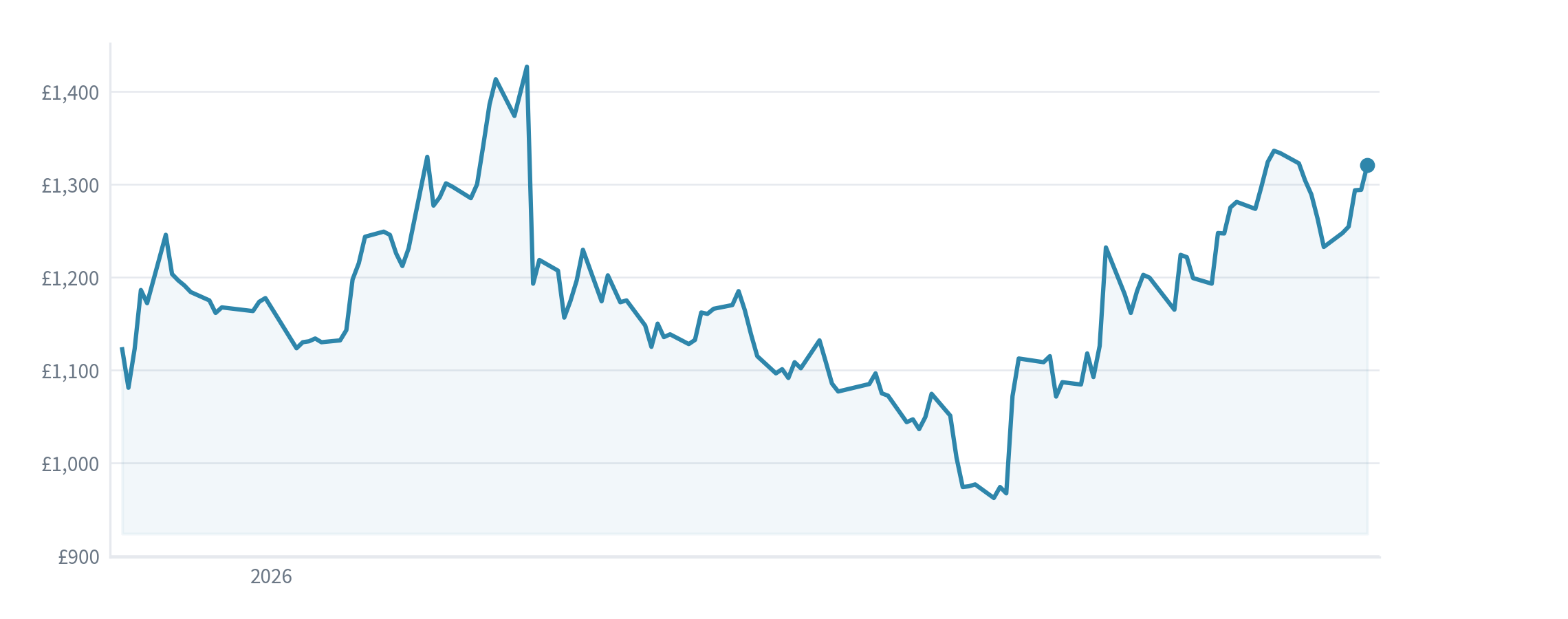

Magnum is the world's largest standalone ice-cream business — it owns Magnum, Wall's, Cornetto and Ben & Jerry's. It was spun out of Unilever in December 2025 as its own separately listed company.

The idea — and why it's parked

There's a real idea here. When a big company spins off a smaller one, index funds and the former parent are often forced to sell the new shares regardless of value, which can push the price below what the business is worth — and that's historically a profitable thing to buy into. Several senior Magnum executives have also been buying shares with their own money (a genuine cluster). But two things stop us acting.

What we think the market is missing — and our honest doubt

The bull case is that the company's cash flow is only temporarily depressed. After the spin, free cash fell about 95% (to roughly €38m) because of one-off separation costs, and the argument is that it recovers toward €800m to €1bn within a couple of years. On normalised cash, that would make it cheap against consumer-staples peers — Nestlé trades at about 17 times next-year earnings, Mondelez about 18 times, Unilever about 14 times. The problem: that recovery is a projection, not yet proven — and ice cream is a genuinely lower-margin business (the reason Unilever let it go).

The set-back / situation, with timing

Beyond the spin, a complication appeared: around 15 May 2026 press reported that Blackstone and CD&R were exploring a takeover of Magnum, and the shares jumped about 12–16% to ~1,260p before fading back to ~1,199p. Crucially, because the spin was structured to be tax-free, Magnum is barred from any takeover for about two years — so that takeover support is largely off the table until ~2027, and buying now would partly be betting on a deal that legally can't happen yet.

The investor checklist (the proven-investor tests)

- Returns on capital / moat — strong brands (a moat), but structurally low ice-cream margins. (mixed)

- Capital allocation — brand-new standalone; heavy debt (about €3bn); a cost-savings programme under way. (a concern)

- Margin of safety — only cheap if the cash recovery happens — and that's unproven. (fails this test)

- Cash quality — free cash down about 95% on separation costs; normalisation not yet evidenced. (fails this test)

- Balance sheet — about €3bn net debt with about €139m of interest to service. (a concern)

- Variant perception + "how could we lose?" — the variant (temporary dip) is unverified, and a takeover-rumour pop has muddied the signal. (fails this test)

- Insider alignment — a genuine senior-executive cluster buying. (pass)

What would make us reconsider

Two clear triggers: (1) the next set of results actually showing free cash recovering as separation costs roll off; or (2) the takeover/tax picture clearing. Until one of those happens, the one good thing (insiders buying) isn't enough on its own, so it stays on the watchlist.

Sources: Unilever demerger materials and the two-year tax restriction; the Blackstone/CD&R bid reports (mid-May 2026); company results showing the separation-cost hit to free cash.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →