RELX

A high-quality, mostly-subscription information business is priced with a nagging worry that AI will make its data free — when in fact RELX's own AI tools are speeding up the growth of its biggest division.

How we would trade it, in plain terms

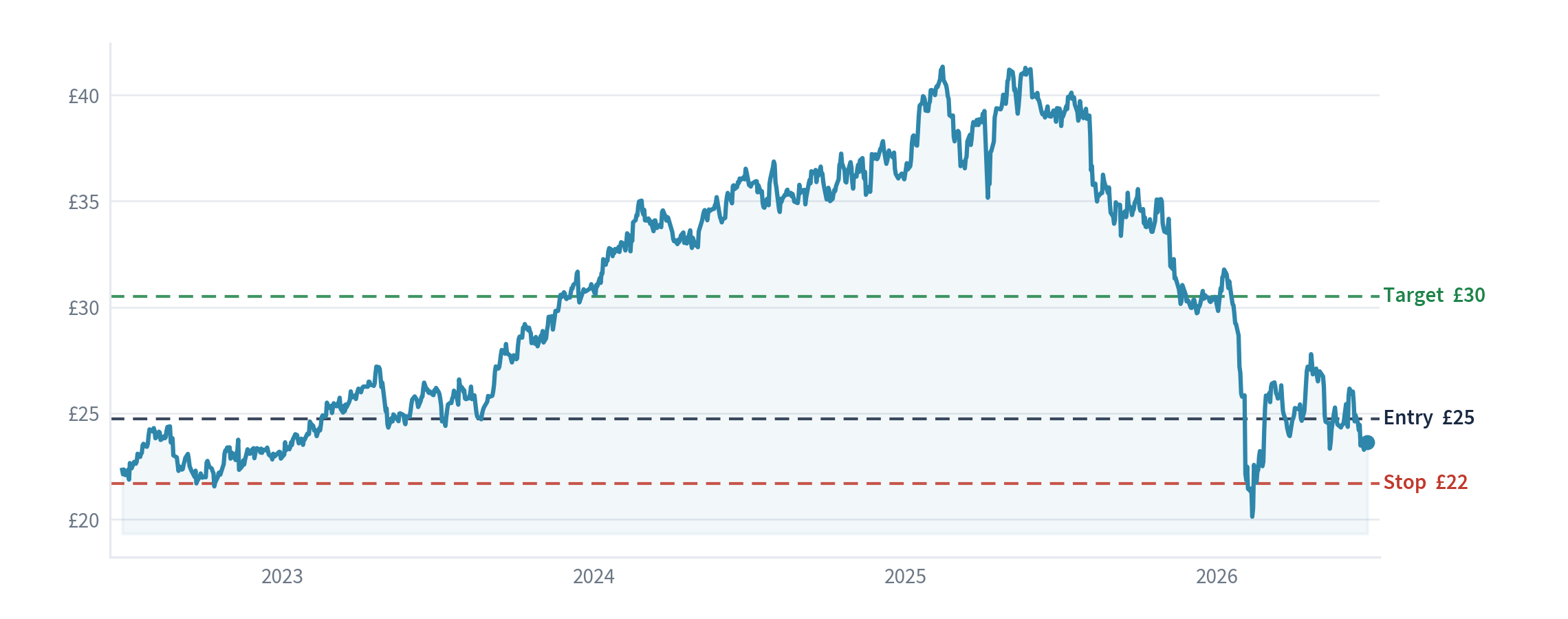

We would buy only on a pullback, via a limit order at £24.75 a share — the shares have run to about £26.16, which thins the reward-to-risk to roughly one-to-one, so we wait for our price rather than chase — and sell and take the loss if it fell to £21.70 (our "stop" — the line that says the idea isn't working), and aim for £30.50 over 12–18 months. That means risking about £3 a share to try to make about £5.75 — roughly two-to-one. Confidence: 3.5 out of 5. A plus for a UK investor: this is a pounds-listed share, so there's no currency drag on the holding the way there is with our US names.

What the company does

RELX sells information and analytics that professionals can't easily do their jobs without: LexisNexis legal research and risk/identity checks, scientific journals and research tools (Elsevier), and large trade exhibitions. About 84% of its revenue is now digital subscriptions — recurring, sticky, and built into customers' daily work, so the income is steady and very profitable.

The idea in one sentence

A high-quality, mostly-subscription information business is priced with a nagging worry that AI will make its data free — when in fact RELX's own AI tools are speeding up the growth of its biggest division.

How shares like this usually behave

Here is our starting point. Subscription-data and workflow businesses are unusually durable — customers build their daily work around them and rarely leave. And the "AI will commoditise information" fear has, so far, proved overstated for owners of proprietary, trusted data (the kind AI tools need licensed access to, rather than replace). That comfort only breaks if AI genuinely disintermediates the data over years. So the odds favour us, but — unlike a one-issue story — RELX carries a stack of slow overhangs (AI, open-access science, and a reputational flare-up), which is why it's the watch name of its tier rather than a top pick.

Why it looks reasonably priced

On about £1.20 of earnings per share, RELX at about £24.75 trades at roughly 21 times earnings. For a business growing earnings about 10% a year on subscription-quality revenue, that is a fair — not stretched — price, and it sits below the priciest data peers: MSCI costs about 39 times earnings, Moody's about 34, and S&P Global about 21 (see our separate note). It isn't a deep bargain; it's quality at a fair price, with a dividend of about 2.7% and a large, growing buyback (raised to £2.25bn for 2026) returning cash on top.

What today's price assumes — and what we think it's worth

We model three possible futures over the next five years. In each we grow the earnings forward, then apply the price-to-earnings ratio we'd expect at the end, to get a fair value:

| Scenario | What we assume | Fair value in 5 years |

|---|---|---|

| Bad case (1-in-4) | AI and open-access science slowly erode the moats; growth fades to mid-single-digit and the rating slips | ~£25 |

| Most likely (1-in-2) | About 10% earnings growth continues and the rating holds near ~21 times | ~£48 |

| Good case (1-in-4) | AI tools keep accelerating the legal arm and the fear fades; the rating edges up | ~£61 |

Blending those three by how likely we think each is gives an expected return of about 14.7% a year, and even the bad case lands roughly at today's price — so with the ~2.7% dividend the downside is small. That makes it strong on a risk-versus-reward basis; the AI-and-open-access overhang is the swing factor.

What we think the market is missing

The bear worry is "AI commoditises information." A year of results says the opposite. In 2025 underlying revenue grew 7%, profit 9% and earnings 10% — a long, steady run — with profit margins rising from about 34% to 35% and all four divisions growing. Most tellingly, the part everyone fears for is accelerating: RELX's own legal AI tools (Lexis+ AI and Protégé) are driving growth of more than 10% a year in the legal division. RELX owns the proprietary, trusted, liability-grade case law and research archives that AI tools need licensed access to and cannot safely make up — so it is positioned as an AI winner, not an AI victim. That is the variant perception.

We are honest that the bear case is live: the shares are down about 32% in 2026, a new AI rival (Anthropic) has reopened the legal-moat debate, and legal-tech spending growth may be slowing. But the data moat is more defensible than a creative-software one, and a great deal of fear is already in the price.

Does the economic backdrop help or hurt?

RELX's revenue is global and subscription-based, so it shrugs off any single economy's cycle — legal, scientific and risk customers keep paying through downturns. The exhibitions arm is the one cyclical piece. For our book it's a pounds-listed holding (no currency drag), though much of the profit is earned in dollars, so a sharply weaker dollar would slightly dent the reported figure.

Why we think there's an edge

Quality at a fair price plus a misread on AI. The durable advantage is the deep switching-cost moat in legal and scientific data. The clearest supporting evidence is in how it spends its cash — a genuine buyback that reduces the share count, plus a growing dividend — and, unusually, in management putting their own money in: both the chief executive and finance chief increased their personal shareholdings during the AI-fear weakness, a real confidence signal. The AI-winner framing is the variant-perception edge. We make no insider-cluster claim beyond those two named purchases.

What other real-world signals show

The ownership picture is reassuring: about 74% institutional ownership (BlackRock the largest at ~11%) and no short-selling or hedge-fund crowd — this is a quiet quality-compounder holding, not a battleground stock. Against that, the risks are stacking beyond AI: open-access science (a slow shift from pay-to-read toward pay-to-publish) pressures the Elsevier journals arm, EU researchers have complained to Brussels about RELX's strong position, and there's a reputational flare-up over a US government data contract. The journals arm is about a third of revenue and open-access is a slow drift, not a cliff — but worth watching. (A fuller sweep of this kind of data is still to come.)

The checklist we run every idea through

- How profitable, and how protected — proprietary legal, scientific and risk data with deep workflow lock-in; high margins and returns on capital; 84% recurring digital revenue.

- What it does with its cash — a £2.25bn buyback that genuinely cuts the share count, plus a growing dividend and disciplined small acquisitions.

- Cushion if we're wrong — about 21 times earnings for a 10%-grower with subscription quality; reasonable, not cheap — said honestly; the ~2.7% dividend adds a small cushion.

- Are the profits real cash? — excellent cash conversion; clean.

- Is it financially solid? — modest, top-tier-rated borrowing.

- Where we differ, and how we could lose — the market fears AI disruption; we see AI acceleration. We lose if AI genuinely undercuts its data over time, or open-access squeezes scientific publishing.

- Are managers aligned with shareholders? — long-tenured management with a strong record, who bought more shares themselves into the weakness.

Management: do they do what they say?

A strong record. Under long-serving chief executive Erik Engstrom (16 years in post), RELX has delivered a remarkably consistent multi-year run of mid-to-high-single-digit growth and steadily rising margins, navigated the shift from print to digital, and is now navigating the shift into AI products. Its record of setting targets and hitting them is among the best in the UK market.

What would make us wrong

The real long-term risk is the bear case being right: if AI genuinely erodes the value of its legal and scientific data over years, the moat narrows and 21 times earnings is too high. Nearer term, an exhibitions downturn or open-access pressure on journals would dent growth. Our discipline: we sell at £21.70 (about 12% below entry).

What we'll watch to check we're right

- The legal arm keeps growing by more than 10% a year on its AI tools (Lexis+ AI, Protégé).

- Overall growth holds near its long-run pace (7% revenue, 10% earnings in 2025).

- The scientific arm's momentum holds despite the open-access drift.

- The buyback and dividend keep returning cash and shrinking the share count.

- What would make us give up: clear evidence AI is taking legal customers, or growth reverting toward mid-single digits — either of those and we'd downgrade or drop it.

- What would make us re-check the whole case: each set of results, fresh moves by AI legal rivals, and any escalation of the open-access or reputational pressures.

Sources: RELX's 2025 full-year results and management commentary; its 2026 buyback and dividend plans; the performance of its legal AI products; recent share-price and ownership data; and market prices for RELX and its data peers. Figures are approximate and for context, not advice.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →