Roper Technologies

A high-quality, mostly-recurring software compounder has quietly fallen about 35% from its highs, and now trades at a sensible price for the first time in years — provided you count its acquisition costs honestly.

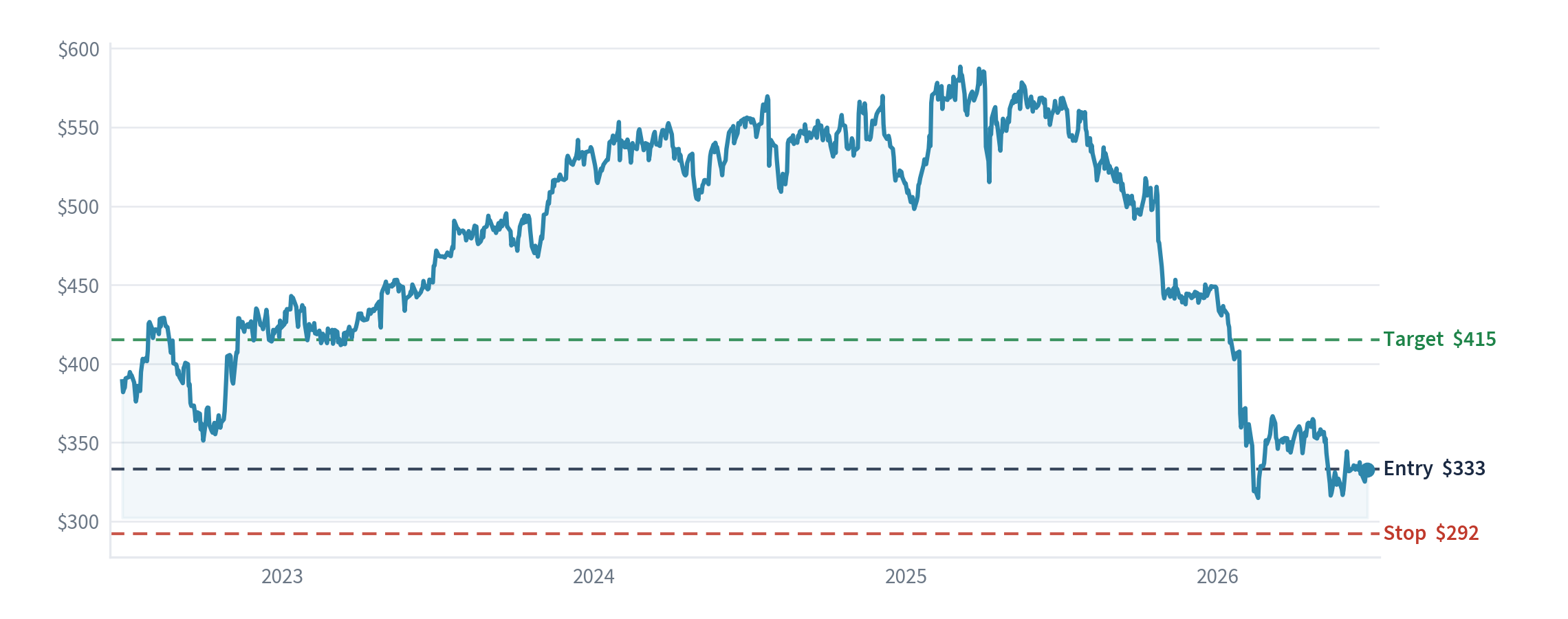

How we would trade it, in plain terms

We would buy at the next day's closing price, about $333 a share, sell and take the loss if it fell to $292 (our "stop" — the line that says the idea isn't working), and aim for $415 over 12–18 months. That means risking about $41 a share to try to make about $82 — roughly two-to-one. Confidence: 3 out of 5, held back because, counted honestly, the shares are fairly priced rather than cheap.

What the company does

Roper is a collection of niche software and technology businesses, each a leader in a small, unglamorous market — software for running law firms, hospitals, construction tenders, freight networks and university research. It buys good businesses, leaves them alone to run well, and uses their cash to buy more. Today it is mostly a software company: well over half its revenue is recurring subscription software, and it sits on about $1.8bn of money customers have already paid for services not yet delivered — a sign of how locked-in the income is.

The idea in one sentence

A high-quality, mostly-recurring software compounder has quietly fallen about 35% from its highs, and now trades at a sensible price for the first time in years — provided you count its acquisition costs honestly.

How shares like this usually behave

Here is our starting point. Serial acquirers that buy software businesses and let them run have a strong long-run record of compounding — the model works, which favours us. The one caveat the base rate flags is how you count the profit: these companies report a flattering "adjusted" figure that adds back the cost of writing down what they buy, so you should never simply take the cheap-looking adjusted price at face value. So the quality is real; the discipline is to judge it on honest earnings.

Why it looks reasonably priced — said honestly

Roper needs an honest valuation note, because the two ways of counting its profit differ a lot:

- On the company's adjusted earnings (about $22 a share guided for this year), Roper at about $333 trades at roughly 15 times earnings — which looks cheap.

- On the stricter all-in earnings (about $14 a share), it trades at about 24 times — which is merely fair.

The gap is the accounting cost of all those acquisitions (writing down the value of what it buys). For a serial acquirer that is a real, recurring cost, so we don't take the cheap 15 at face value — the truth sits between the two, and management itself points to free cash flow (the spare cash left after the bills) as the honest gauge. Even so, against peers Roper looks fairly-to-attractively priced: Ametek about 24 times, Danaher about 24, and pure software compounders higher still. The clincher is that Roper has fallen about 35% from its recent highs — for the first time in years you can buy this compounder without paying a peak price.

What today's price assumes — and what we think it's worth

We model three possible futures over the next five years. In each we grow the earnings forward, then apply the price-to-earnings ratio we'd expect at the end, to get a fair value:

| Scenario | What we assume | Fair value in 5 years |

|---|---|---|

| Bad case (1-in-4) | Organic growth fades and acquisitions start to disappoint; the honest-earnings rating stays full | ~$332 |

| Most likely (1-in-2) | About 6% organic growth plus steady, sensible acquisitions, and recurring software keeps compounding | ~$550 |

| Good case (1-in-4) | The acquisition pipeline delivers and the AI features start earning money; the rating recovers | ~$779 |

Blending those three by how likely we think each is gives an expected return of about 10.4% a year, with a worst-case loss of only about 0.4% — an unusually small downside, because the recurring revenue and the recent 35% fall already cushion the shares.

What we think the market is missing

The market has lumped Roper in with industrial "acquisition roll-ups" that are running out of room. But its results behave like a software compounder: latest-quarter revenue grew 11% (about 6% from the existing businesses, the rest from acquisitions), recurring software revenue grew 7% — which management calls its best single indicator of health — free cash flow grew by more than 10%, and management raised its full-year guidance while buying back $1.5bn of its own (now cheaper) stock. Underneath, the businesses are genuinely sticky — more than 95% of customers stay each year — and Roper is shipping AI features across its products. A business compounding cash like this, finally available at a non-stretched price, is the opportunity; and the recent stress among private buyers is freeing up quality businesses for Roper to acquire on better terms.

Does the economic backdrop help or hurt?

Roper's software runs essential back-office functions (legal, healthcare, logistics, education), so demand is sticky and barely cyclical, which supports the thesis. Because it earns in US dollars, the dollar-to-pound exchange rate affects what we make in pounds, and lower interest rates would help both the value the market puts on it and the maths of its acquisitions. No single government policy is decisive.

Why we think there's an edge

This is a quality compounder at a now-reasonable price. The durable advantages are deep, recurring-revenue moats across dozens of niche-leading software businesses, and a proven record of compounding through disciplined acquisitions — now paired with genuine buybacks at a cheaper price (the share count really falls). These are independent of the recent de-rating. There is a supporting insider signal: the chief executive made a discretionary open-market purchase of about $4.5m after the shares fell (he holds around $67m). It reached us through a quality investor's holdings, but the case rests on the business and the price.

What other real-world signals show

The signals are net-positive with a clear caveat. Analysts' forecasts are being revised up (recent profit estimates raised, none cut), and the typical price target sits well above today's price. But about 21% of analysts still rate it a sell — reflecting the very adjusted-versus-honest-earnings debate we flagged. So the momentum is positive while the valuation debate persists. (A fuller sweep of this kind of data is still to come.)

The checklist we run every idea through

- How profitable, and how protected — dozens of niche-leading, high-recurring software businesses, with more than 95% of customers staying each year; high cash returns on the capital actually used in the units.

- What it does with its cash — the whole model is disciplined acquisition; now also buying back stock at a marked-down price.

- Cushion if we're wrong — fairly priced on honest earnings (~24 times), cheap on adjusted (~15), and about 35% off its highs; the de-rating is the cushion (the modelled bad case barely loses money).

- Are the profits real cash? — strong free cash flow and a large pool of pre-paid revenue; the one honest flag is the gap between adjusted and all-in earnings, which we account for by leaning on cash flow.

- Is it financially solid? — carries debt to fund acquisitions, but it's comfortably covered by the recurring cash.

- Where we differ, and how we could lose — the market sees a tiring roll-up; we see a software compounder on sale. We lose if organic growth fades and acquisitions start to disappoint or overpay.

- Are managers aligned with shareholders? — long-tenured, capital-allocation-focused management; the chief executive bought shares himself after the fall.

Management: do they do what they say?

A strong record. Under chief executive Neil Hunn (in post since 2018), Roper has one of the better long-run records of saying what it will earn and delivering, with a disciplined, repeatable acquisition method (about $3.3bn deployed last year); the latest quarter beat and management raised full-year guidance. The tone is specific and numbers-led, and management itself points investors to cash flow rather than the flattering adjusted figure — which is the honest thing to do.

What would make us wrong

If organic growth slips and the acquisition engine starts overpaying or buying weaker businesses, the compounding stops and even 15 times adjusted earnings is no bargain. A sharp rise in interest rates would also hurt both the valuation and the acquisition maths. Our discipline: we sell at $292 (about 12% below entry).

What we'll watch to check we're right

- Recurring software revenue keeps growing (it rose 7% — management's key health gauge).

- Free cash flow keeps compounding by more than 10% a year (the honest measure of profit here).

- Acquisitions stay disciplined and keep adding to earnings on sensible terms.

- Customer retention stays above 95%.

- What would make us give up: organic growth fading with acquisitions starting to disappoint or overpay — that and we'd downgrade or drop it.

- What would make us re-check the whole case: each quarter's results and cash flow, and any large or richly-priced acquisition.

Sources: Roper's results announcement and investor call for its latest quarter and its raised full-year guidance; its recurring-software, retention and cash-flow disclosures; the financial figures it files with the US regulator; recent analyst notes and estimate revisions; and market prices for Roper and its peers (Ametek, Danaher). Figures are approximate and for context, not advice.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →