S&P Global

One of the best toll-booth businesses in finance — ratings and indices that almost everyone has to pay to use — is reasonably priced, growing by more than 10% a year, and about to unlock value by spinning off a division just weeks from now.

How we would trade it, in plain terms

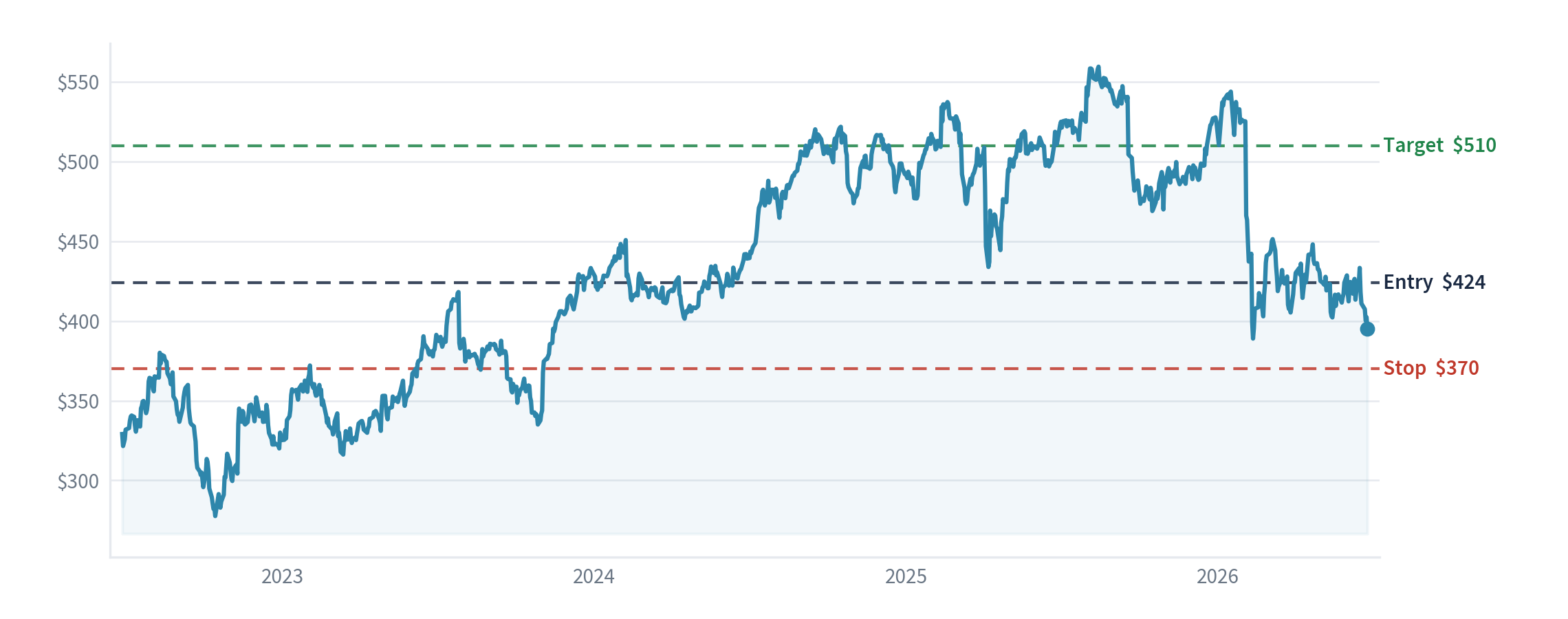

We would buy at the next day's closing price, about $424 a share, sell and take the loss if it fell to $370 (our "stop" — the line that says the idea isn't working), and aim for $510 over 12–18 months. That means risking about $54 a share to try to make about $86 — about 1.6 to one at today's slightly higher price. Confidence: 4 out of 5, our highest in the current pool. One mechanic to know: if you still hold the shares on 1 July 2026, you will receive shares in a business being spun off (one share of "Mobility Global" for each S&P Global share), so part of the value arrives as a separate holding rather than in the S&P Global price.

What the company does

S&P Global is one of only two companies in the world (with Moody's) that rate how likely a borrower is to pay back its bonds. Almost every large bond sold has to carry a rating, so it is close to an unavoidable toll on borrowing. It also owns the S&P 500 and Dow Jones share indices — it earns a small fee every time money is invested to track them — plus a large financial-data business and the Platts energy price benchmarks. It is about to spin off its Mobility division (car data and the CARFAX vehicle-history service), leaving behind a cleaner, even higher-margin ratings-data-and-indices company.

The idea in one sentence

One of the best toll-booth businesses in finance — ratings and indices that almost everyone has to pay to use — is reasonably priced, growing by more than 10% a year, and about to unlock value by spinning off a division just weeks from now.

How shares like this usually behave

Here is our starting point. Wide-moat ratings and index franchises rarely fall out of favour for long: the work is recurring, the customers can't easily switch, and the profits compound. And a value-unlocking spin-off — splitting a company in two so the market can value each half properly — is a setup our own record rates well, because the cleaner, faster-growing piece usually re-rates higher once it stands alone. The risk to that pattern is a genuine downturn in how much the world borrows, which is the one thing that slows the ratings engine. So the odds are firmly on our side, with one clear thing to watch.

Why it looks cheap

On this year's expected profit (about $19.50 of earnings per share), S&P Global at about $417 trades at roughly 21 times earnings. That is a clear discount to the businesses it most resembles: Moody's, its ratings twin, costs about 34 times earnings, and MSCI, the index-and-analytics company, about 39 times. For two of the finest toll-booth franchises in finance, paying 21 times when the near-identical Moody's commands 34 is the opportunity. And unlike those two, S&P Global has a catalyst on the calendar — the 1 July spin-off — that should let the market value the cleaner remaining company more highly, while the spun-out Mobility business (which earns about 45 pence of profit on every pound of sales) gets its own price.

What today's price assumes — and what we think it's worth

We model three possible futures over the next five years. In each we grow the earnings forward, then apply the price-to-earnings ratio we'd expect at the end, to get a fair value:

| Scenario | What we assume | Fair value in 5 years |

|---|---|---|

| Bad case (1-in-4) | A borrowing recession stalls ratings and the data arm keeps losing ground; earnings barely grow and the rating slips to ~18 times | ~$407 |

| Most likely (1-in-2) | 6–8% growth a year, the spin works, and the cleaner company holds ~25 times | ~$754 |

| Good case (1-in-4) | Strong bond issuance plus the AI tailwind below; the rating rises toward ~30 times | ~$962 |

Blending those three by how likely we think each is gives an expected return of about 12.3% a year, with a worst-case loss of only about 2.4% — the best risk-versus-reward balance in our whole pool. In plain terms: at 21 times earnings the downside is well protected, because even the bad case lands close to today's price, while the catalyst and the quality give real upside.

What we think the market is missing

The recent worry was that S&P Global's data arm, Market Intelligence, would be "commoditised" by AI — that free or cheap AI tools would undercut what it sells. A close read of a year of results says the opposite. Management spells out that less than 5% of revenue is the kind of plain, undifferentiated data AI could replace — most of it is proprietary data, workflow software customers build their daily work around, and advisory — and that clients are paying 35–45% more to renew when AI access is added. That is pricing power, not price erosion; the data arm still grew about 8%. Meanwhile the crown-jewel ratings business grew 13%, helped by an unexpected source — the huge debt the big cloud-computing companies are raising to build AI data centres — and by booming private-credit lending, where ratings revenue rose about 25%. The market priced a victim of AI; the evidence shows a business getting paid more because of it.

The one honest headwind: management expects ratings growth to slow later in 2026 and turn slightly negative in the final quarter, simply because it is being compared with an exceptionally strong prior year — a known arithmetic bump, not a broken moat.

Does the economic backdrop help or hurt?

The ratings business rises and falls with how much debt the world is issuing, so falling interest rates (which encourage more borrowing) help it, and rising rates hurt it. The index business earns more as markets rise and more money tracks the S&P 500. Both are broadly supported right now. Because S&P Global earns in US dollars, the dollar-to-pound exchange rate affects what we make in pounds.

Why we think there's an edge

This is a quality business at a discount with a dated catalyst — two separate reasons to win, which is the combination we look for. The first is the spin-off on 1 July, a concrete corporate event that should let the market value the cleaner company properly. The second is the valuation gap — toll-booth franchises at 21 times earnings against near-identical peers at 34–39. The clearest supporting evidence is in how management is spending its cash: they raised buybacks to at least 100% of the spare cash the business throws off (about $4.5bn a year) specifically because they think the shares are cheap, and the new chief executive bought shares in the open market herself. It reached us through a concentrated quality investor's holdings, but the case rests on the business and the catalyst, not on whose holdings it appeared in.

What other real-world signals show

The outside signals are supportive. Professional analysts are firmly behind it — about 93% rate the shares a buy, and several lifted their price targets (Goldman Sachs, JPMorgan, Wells Fargo, Mizuho), with a typical target around $543, roughly 30% above today. The one amber flag is that some analysts trimmed their near-term forecasts on the softer data-arm revenue — the same point we are watching. (A fuller sweep of this kind of data is still to come.)

The checklist we run every idea through

- How profitable, and how protected — ratings and index licensing are among the widest moats in finance (rules entrench them, and the S&P 500 is a brand in its own right); very high margins and returns on capital.

- What it does with its cash — steady buybacks and dividends, now raised to at least all of the spare cash generated, plus the spin-off itself as a deliberate value-unlock.

- Cushion if we're wrong — 21 times earnings for a company growing more than 10% a year, trading well below its twin at 34; the modelled bad case loses only about 2%.

- Are the profits real cash? — yes; recurring, subscription-like revenue that converts cleanly to cash.

- Is it financially solid? — strong, top-tier credit; no balance-sheet risk.

- Where we differ, and how we could lose — the market lumps it in with slower financial firms; we see a cleaner, faster toll-booth after the spin. We lose if global borrowing dries up and the spin disappoints.

- Are managers aligned with shareholders? — held by a proven concentrated investor; the chief executive bought shares herself. No wider insider-buying claim is made.

Management: do they do what they say?

A strong record. S&P Global has a long history of steady, guidance-meeting delivery, absorbed the large IHS Markit takeover, has raised its guidance, and is delivering the Mobility separation exactly on the timetable it set. The new chief executive, Martina Cheung (in post since late 2024, promoted from within after running both the ratings and the data arms), bought shares in the open market and sold none — a genuine, owner-aligned signal of confidence. The tone is specific and numbers-led.

What would make us wrong

The real risk is the economy, not the price. A sharp slowdown in global borrowing — a recession or a fresh spike in interest rates — would slow the ratings engine, and a market downturn would dent index fees. If the spin-off is received poorly, or the remaining company simply doesn't re-rate, the catalyst fizzles. Our discipline: we sell at $370 (about 13% below today's price), roughly where "borrowing has genuinely stalled" would be winning the argument.

What we'll watch to check we're right

- The spin-off completes on 1 July — Mobility lists as Mobility Global (New York Stock Exchange, ticker: MBGL), and shareholders receive their new shares.

- The remaining company re-rates toward its peers once it stands alone.

- Ratings growth holds up outside the known final-quarter comparison bump.

- The data arm keeps lifting prices on AI-enabled renewals, rather than losing ground.

- What would make us give up: a real downturn in global bond issuance, or the data arm starting to shrink on price — either of those and we'd downgrade or drop it.

- What would make us re-check the whole case: each quarter's results, the completion of the spin, and any sign that borrowing is rolling over.

Sources: S&P Global's results announcements and investor calls for its last several quarters; its 2026 financial guidance; the official documents and timetable for the Mobility spin-off (shares distributed 1 July 2026, one Mobility Global share per S&P Global share); the financial figures the company files with the US regulator; recent analyst notes and price targets; and market prices for S&P Global, Moody's and MSCI. Figures are approximate and for context, not advice.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →