Veralto

A boring-but-essential, mostly-recurring business with a proven compounding model is trading at a clear discount to the other high-quality "water and testing" companies it sits alongside.

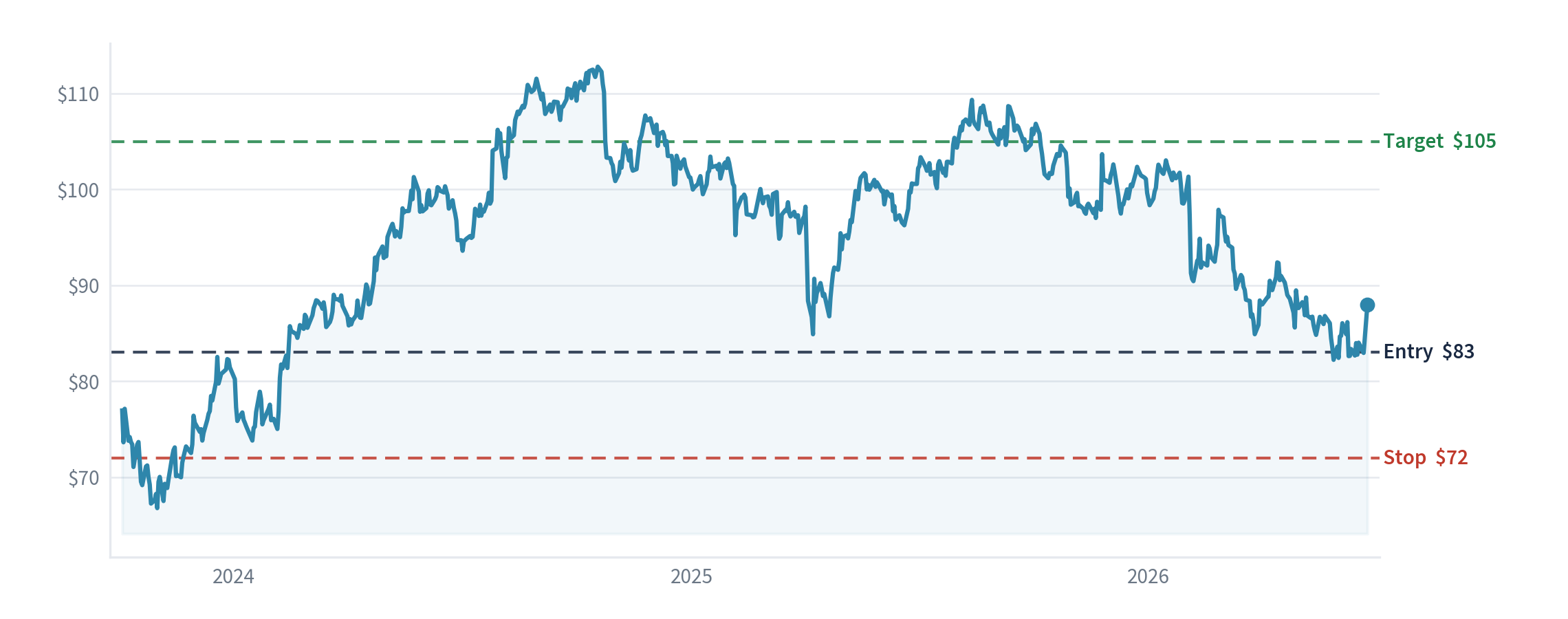

How we would trade it, in plain terms

We would buy at the next day's closing price, about $83 a share, sell and take the loss if it fell to $72 (our "stop" — the line that says the idea isn't working), and aim for $105 over 12–18 months. That means risking about $11 a share to try to make about $22 — roughly two-to-one. Confidence: 3.5 out of 5, held a touch back because its underlying ("organic") growth is only low single digits.

What the company does

Veralto sells the instruments and consumables that keep water safe and products correctly labelled. It has two halves: Water Quality — the kit cities and factories use to test and treat water, plus the chemicals and parts they must keep rebuying — and Product Quality — the machines that print use-by dates and codes on packaging and check they're right. The crucial feature is that about 62% of sales are recurring: once a customer installs a Veralto system, they buy its consumables and service for years. It was spun out of Danaher in 2023 and runs the same buy-good-businesses-and-improve-them method.

The idea in one sentence

A boring-but-essential, mostly-recurring business with a proven compounding model is trading at a clear discount to the other high-quality "water and testing" companies it sits alongside.

How shares like this usually behave

Here is our starting point. Two patterns favour us. First, spin-offs from serial acquirers like Danaher tend to compound well once they stand alone with their own incentives — it's a setup our own record rates highly. Second, a quality business priced below its direct peers usually closes some of that gap over time. The risk to both is simple: if the underlying growth stays stuck near zero, the "discount" turns out to be deserved. So the odds favour us, with the growth rate as the thing to watch.

Why it looks cheap

On this year's profit guidance (about $4.24 of earnings per share), Veralto at about $83 trades at roughly 20 times earnings. Its closest high-quality peers cost meaningfully more: Danaher, its former parent, about 24 times; Mettler-Toledo, the testing-instrument maker, about 26; Xylem, in water, about 28; and Ecolab, in water treatment, about 30. For a business with the same recurring-revenue quality and the same Danaher method, 20 times is the cheapest in the room — and that discount is the opportunity. Veralto also earns a high 25% operating margin, turns profit into cash well, and has a clean balance sheet that lets it keep buying small businesses to grow (it spent about $1bn on two of them this year).

What today's price assumes — and what we think it's worth

We model three possible futures over the next five years. In each we grow the earnings forward, then apply the price-to-earnings ratio we'd expect at the end, to get a fair value:

| Scenario | What we assume | Fair value in 5 years |

|---|---|---|

| Bad case (1-in-4) | Underlying growth stays stuck near zero and the acquisition engine slows; the rating stays near today's ~20 times | ~$75 |

| Most likely (1-in-2) | Low-single-digit core growth plus steady acquisitions, the rating holds | ~$137 |

| Good case (1-in-4) | Water demand from data centres and chip plants lifts growth, and the rating rises toward its peers | ~$187 |

Blending those three by how likely we think each is gives an expected return of about 9.6% a year, with a worst-case loss of about 10%. Solid rather than spectacular — the low underlying growth rate is exactly what caps it, and also what makes it cheap.

What we think the market is missing

The market files Veralto under "slow industrial" because its organic growth is only about 2%. Two things look under-appreciated. First, the recurring base makes the earnings unusually dependable — a quality that deserves a premium, not a discount, to ordinary industrials. Second, the demand drivers are quietly picking up: industrial water demand is being pulled along by data centres, semiconductor plants and power stations, all of which need a lot of clean, monitored water. Encouragingly, management raised its full-year guidance at the latest quarter and expects growth to speed up through the year, with the strong half (Water Quality, up about 10%) carrying a small drag in the more cyclical Product Quality half. A dependable compounder with a strengthening end-market shouldn't trade below its peers.

Does the economic backdrop help or hurt?

Water quality and safety are regulated necessities, so demand barely moves with the economic cycle, and tightening environmental rules (for example on "forever chemicals" in water) are a slow tailwind — though they can also mean extra spending for Veralto's customers. The newer pull from data-centre and chip-plant construction is a genuine growth kicker. Because Veralto earns in US dollars, the dollar-to-pound exchange rate affects what we make in pounds, and lower interest rates would modestly help the value of a steady compounder like this.

Why we think there's an edge

This is a spin-off plus quality-at-a-discount idea — two independent reasons to win. The first is the spin-off itself: a Danaher carve-out running the proven Danaher method, with fresh standalone incentives. The second is the valuation gap to peers, which gives the margin of safety. The compounding engine is disciplined small acquisitions funded by strong cash flow. We make no insider-buying claim — in fact the chief executive has been a net seller (below), so we lean on the model and the price.

What other real-world signals show

The signals are mixed-to-cautious, consistent with the slow-growth limiter. Short-selling is very low (around 1.8% and falling — no bear thesis in the market), but some analysts trimmed their forecasts and targets (RBC, Citi) and the consensus is a "hold." Reassuringly, the recent drag is concentrated in one segment (the cyclical Product Quality half, down about 1%) while the larger Water Quality half keeps growing — so it's a specific, identifiable issue, not whole-company weakness, and there are no accounting red flags. (A fuller sweep of this kind of data is still to come.)

The checklist we run every idea through

- How profitable, and how protected — about 62% recurring revenue, 25% operating margins, and an entrenched installed base of regulated, mission-critical kit that's painful to switch out.

- What it does with its cash — strong cash flow funnelled into disciplined small acquisitions (the Danaher model), plus opportunistic buybacks.

- Cushion if we're wrong — about 20 times earnings for a recurring-revenue compounder whose peers cost 24–30; the discount is the safety margin.

- Are the profits real cash? — yes; high cash conversion.

- Is it financially solid? — modest borrowing, plenty of room to keep acquiring.

- Where we differ, and how we could lose — the market sees a slow industrial; we see a dependable compounder with a strengthening end-market, mispriced versus peers. We lose if growth stays stuck near zero and the acquisition engine stalls.

- Are managers aligned with shareholders? — experienced ex-Danaher management; no insider buying (the chief executive has been a net seller).

Management: do they do what they say?

A good early record on a short history. Chief executive Jennifer Honeycutt spent 20-plus years running Danaher businesses and has executed the spin-off well — steady results and a raised full-year guidance at the latest quarter, while deploying about $1bn into sensible acquisitions. The honest caveat: the standalone history is short (spun out only in 2023), and she has been a net seller of her own shares (though she still holds about $11m), so there's no insider-buying signal here. We lean on the Danaher pedigree and the early evidence.

What would make us wrong

If underlying growth stays stuck near zero and the acquisition machine slows or overpays, then a low-growth industrial deserves a low-growth rating and the "discount" isn't really one. A sharp industrial downturn would also hit the roughly 38% of sales that aren't recurring. Our discipline: we sell at $72 (about 13% below entry).

What we'll watch to check we're right

- Underlying growth accelerates through 2026, as management guided.

- The Water Quality half keeps leading, and the cyclical half stops dragging.

- Acquisitions stay disciplined and keep compounding earnings.

- The valuation gap to peers narrows.

- What would make us give up: growth stuck near zero with the acquisition engine stalling — that and we'd downgrade or drop it.

- What would make us re-check the whole case: each quarter's results, any change in the water-demand drivers, and the pace of acquisitions.

Sources: Veralto's results announcements and investor call for its latest quarter and its raised 2026 guidance; its recent acquisitions; the financial figures it files with the US regulator; recent analyst notes; and market prices for Veralto and its peers (Danaher, Mettler-Toledo, Xylem, Ecolab). Figures are approximate and for context, not advice.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →