WEX Inc

A solid, cash-generating company is being priced as though it is slowly dying — and at the same time its own senior managers are spending their own money buying the shares.

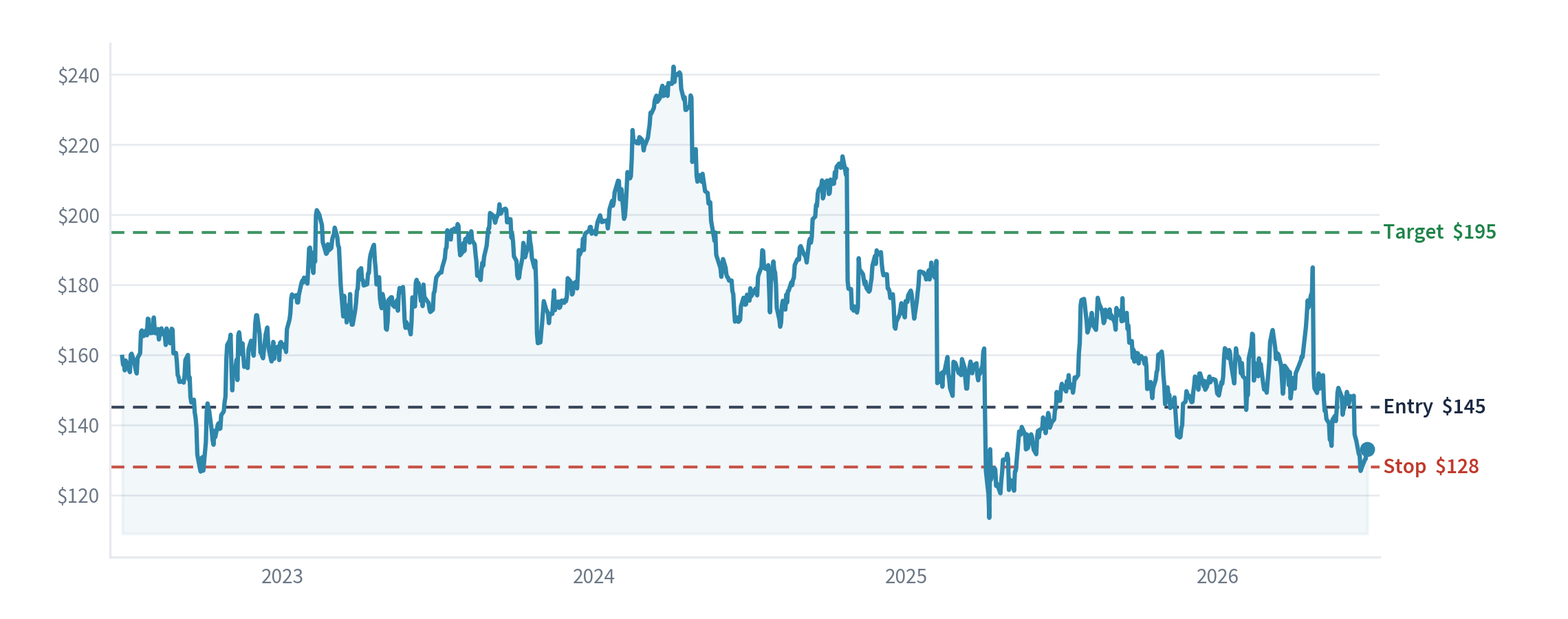

How we would trade it, in plain terms

We would buy at the next day's closing price, which is currently about $145 a share. We would sell and accept the loss if the price fell to $128 (this is our "stop" — the line that tells us the idea isn't working). Our goal price is $195, which we'd expect to take 12–18 months to reach. That means we are risking about $17 a share to try to make about $50 — roughly three times as much potential gain as loss, which is the kind of balance we want before committing. Our confidence is 4 out of 5.

What the company actually does

WEX is, in simple terms, a payments company. Three things pay its bills. First, it runs fuel cards and payment systems for company vehicle fleets — when a delivery firm's drivers fill up, WEX handles the payment and takes a small fee. Second, it handles payments between businesses (paying suppliers, invoices and so on). Third, it administers health and benefit accounts for employees. None of this is glamorous, but it is repetitive, fee-based business that produces a lot of cash.

The idea in one sentence

A solid, cash-generating company is being priced as though it is slowly dying — and at the same time its own senior managers are spending their own money buying the shares.

Why we think it is cheap

The simplest measure of "cheap or dear" is the price-to-earnings ratio — how many dollars you pay for each dollar of yearly profit. WEX trades at about 7 — you pay roughly $7 for every $1 of expected annual profit. To judge whether that is genuinely cheap we have to compare it with similar companies, so here is the like-for-like picture:

- WEX: about 7 times

- Corpay (its closest large rival): about 12 times

- Fidelity National Information Services: about 6 times

- Global Payments: about 5 times

Being honest, this tells a mixed story: WEX is clearly cheaper than Corpay, the company it most resembles, but the whole payments industry is currently out of favour, so WEX is not the single cheapest name. The stronger point is cash. After paying everything it needs to keep running, WEX generates roughly $671 million of genuine spare cash a year ("free cash flow"). Against a company worth about $5 billion on the stock market, that is about a 13% cash return each year — a high figure, and the part of the case we lean on most. The company is also genuinely returning that cash: it has bought back enough stock to cut its share count from about 43 million to 34 million over three years (down roughly 21%). We check this deliberately, because some firms "buy back" shares only to cancel out new ones handed to staff — here the count is really falling, so each remaining share owns more of the business. (We also deliberately avoid a popular profit shorthand that flatters companies by ignoring real costs like interest and tax; we prefer the actual cash and the actual profit.)

What we think the market is missing

Current pricing is fixated on one weak part of the business — corporate payments — which lost a large customer and has missed its own targets. We think that worry is overshadowing the bigger, better news: the company's cash generation has clearly turned upward. In the most recent quarter, free cash was almost three times what it was a year earlier, and management actually raised its forecast for the year. So the part everyone is worried about is shrinking, while the parts that matter are getting stronger — and the share price has not caught up.

The signal we are acting on (and why it counts)

Our trigger here is insider buying — by a cluster, not one person. In February 2026 a broad group of WEX's most senior people — the chairman, the finance chief, the operating chief and several others — bought shares on the open market with their own money, at around $143, very close to today's price. One executive buying can mean little; a whole group buying together, near the lows, has historically been one of the more reliable signs that the people who know the business best think it is undervalued. We track this signal specifically so we can learn, over time, whether it pays off for us. Separately, an activist investor won seats on the board, which usually leads to more disciplined spending of the company's cash.

The investor checklist (the proven-investor tests)

- Returns on capital — high (around 30%): a genuinely good business, not just a cheap one.

- Use of cash — real buybacks (share count down about 21% in three years) plus a newly disciplined board.

- Margin of safety — cheaper than its nearest peer, with about a 13% annual cash yield.

- Cash quality — strong free cash; we use the company's own figure, not the inflated screener one.

- Balance sheet — carries a lot of debt, but it's a payments lending model and the cash easily covers it — one to watch.

- What others believe that we don't — they price terminal decline; the weak division is shrinking while the cash engine accelerates.

- Insider alignment — a broad, multi-executive open-market cluster.

Management track record (do they do what they say?)

Medium. Over the last year they have done what they said — they raised their forecast through 2025 and then beat it again in early 2026. They were also honest about a difficult 2024 (when a large travel-payments customer pulled work in-house, they acknowledged the hit rather than spinning it), and they ran a full review and decided against breaking the company up. It's only "medium" because that 2024 stumble is still fairly recent and today's optimism leans partly on a recovering fuel and travel backdrop, so the guidance is measured rather than blue-sky.

What would make us wrong

The honest bear case is simple: if the weak corporate-payments division keeps shrinking and drags the whole company's growth down with it, then the low price is deserved, not a bargain. There is also a fair amount of debt on the books — though for a payments company that funds a lending book, that is normal, and the cash easily covers it. If the shares fell to $128 we would accept we were wrong and step aside.

Sources: WEX's first-quarter 2026 results; the activist (Impactive) board agreement; the insider share-purchase filings. Figures are approximate and for context, not advice.

Part of an open research-framework experiment — generic research, not a personal recommendation and not advice. The entry, stop and target are the framework's own tracked levels, not instructions or predictions for you. The book is hypothetical (notional money, no trades placed); capital is at risk and past or hypothetical performance is not a reliable indicator of future results. Portfolio Lab is not FCA-authorised. Disclosures & risk →